Creation date : 15/06/2018

Angela, 48, has always naturally thought about the future.

When she bought her two-room apartment right in the centre of Luxembourg City, she thought about her children first.

“I was reassured to know that they wouldn't be in debt if something happened to us", she says.

To finance their apartment, Angela and her husband had requested a loan of 700,000 euros.

The bank agreed this with them under the condition of taking out a Remaining Due Balance insurance covering the total amount of the loan.

This is a term insurance, limited to the repayment term.

The paid-up capital in the event of death corresponds to the balance of the loan.

"This insurance allows us to get a good night's sleep. If something dramatic happened to us, such as death or an accident that would prevent us from working, the insurance would take over to pay our monthly loan instalments, explains Angela.

Different packages in remaining due balance insurance

Alejandro also preferred to buy his home in Luxembourg.

His bank demanded an insurance policy covering 100% of the borrowed capital.

"This capital decreases each year based on the repayments we have already made", he explains.

Calculated on a case-by-case basis, the insurance premium takes into account the amount of the loan (the greater the capital to be insured, the higher the premium), the interest rate and the duration of the loan.

Insurance companies also evaluate the risk of death: age(s) of the insured party(ies), state of health, profession, whether they practice risky sports, etc...

"We had the choice either to pay a single premium that we included in the loan amount or pay annual premiums.

We opted for the single premium because it allowed us to deduct it from our taxes and it also worked out cheaper ", advises Alejandro.

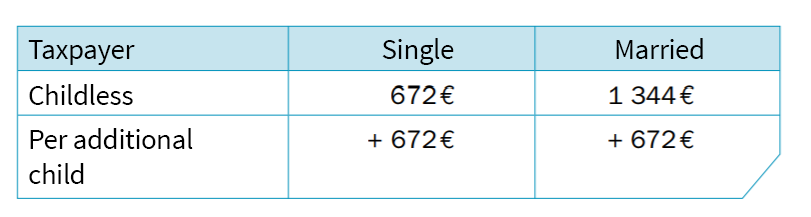

A tax-deductible premium

Remaining Due Balance insurance premiums are tax deductible from income up to a ceiling of 672 euros per year, and double that if you are married or per additional child.

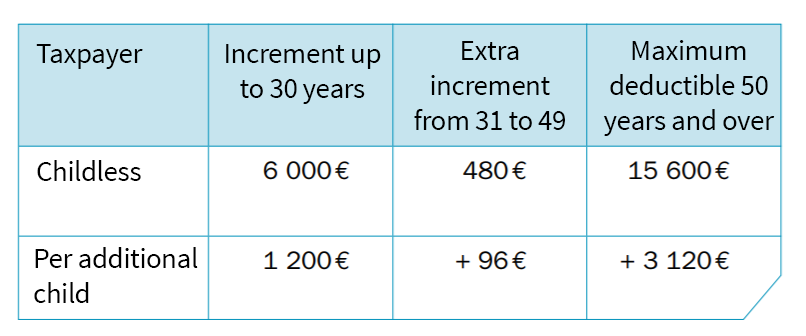

In case of payment by a single premium, the annual deductible limit increases.

The Luxembourg government's direct contributions authority offers examples of calculations of tax deductions from the single premium. For more information, do not hesitate to consult the 2021 Luxembourg tax guide !

Protection available from your insurer

These Remaining Due Balance insurance policies are offered by banks as part of a global package for your real estate project. Be aware that the bank cannot demand that this insurance be taken out with them.

Also compare prices, they may be more beneficial with insurance professionals