Creation date : 30/12/2019

Two different motor no-claims bonus scales:

The ‘bonus-malus’ system is used in all European countries but in different ways. In Luxembourg, most insurers use two different scales.

- The first scale covers Civil Liability and concerns accidents you cause to a third party. The ‘bonus-malus’ scale for Civil Liability is governed by Luxembourg law. It is calculated in the same way by all insurers nation-wide.

- The second scale covers Material Damage, i.e. the damage caused by you or by an unidentifiable third party to your own vehicle. Here, the application, or not, of a ‘bonus-malus’ is left to the discretion of each insurer.

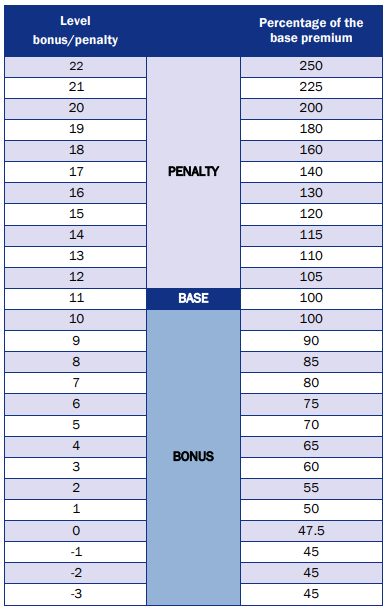

Understanding the statutory motor ‘bonus-malus’

The Civil Liability ‘bonus-malus’ scale has 25 levels numbered from 22 to - 3. - 3 corresponds to the maximum bonus and 22 to the maximum possible penalty.

If you are insuring a vehicle for the first time, you start in the middle of the ‘bonus-malus’ scale, i.e. at 11, the basic degree that corresponds to an insurance premium rate of 100%.

Then, every year without an accident takes you down a notch on this scale. For example, after 4 years without an accident, your Civil Liability bonus is 7.

On the other hand, if you cause an accident, you climb 3 points on the Civil Liability ‘malus’ scale. This means that if you started off at the basic level (11), you will be at 14 the following year.

Note that each time you climb up or down the Civil Liability scale, part of your premium changes: only the amount that corresponds to the Civil Liability insurance cover. The amount related to your other insurance cover (theft, fire, etc.) does not change. This has the advantage of making the penalties (malus) less severe than in some other countries where insurers increase the entire premium.

Retaining or transmitting your Civil Liability bonus

Your degree of bonus-malus is non-transferable It is therefore impossible to insure a second car with the same bonus or to allow your family and friends to benefit from it.

All insurers operating in Luxembourg are subject to the same rules. A good thing when you want to change insurers in Luxembourg. All you need to do is to present a ‘bonus-malus’ certificate provided by your last insurer. Your new insurance company is required by law to apply the same level.

Insuring your car for the first time in Luxembourg

You are moving to the Grand Duchy and would like to keep the bonus already earned in another country? Even if the scales differ, equivalences exist with neighbouring countries such as France and Belgium, Germany and even Portugal.

Not from Luxembourg? Present your ‘bonus-malus’ certificate issued by the insurer of the country you are leaving. Insurers consider these requests on a case-by-case basis and may grant you discounts. As long, of course, as the insurance certificate in another country is issued in your name.

Material damage and other types of insurance cover

Without being a legal obligation, many insurers in Luxembourg - including AXA - apply the same scale system to the "material damage" part of your insurance.

Other types of insurance cover, such as assistance in the event of a breakdown or legal protection, are completely free of ‘bonus-malus’ scales. The premiums you will be charged for this insurance cover remain stable, regardless of your risk profile.